Peter

An “Unconventional” Future for Natural Gas in the United States

Growing demand for energy in the United States is causing shifts in the mix of fossil fuel supplies and creating new opportunities for geological research. Oil, gas and coal are the country’s primary energy sources. Yet the United States faces declining domestic oil production and increasing reliance on oil imports: According to the U.S. Department of Energy (DOE), the United States already imports 67 percent of the oil it consumes. And though we have plenty of coal, it has a bad reputation for not being clean. Natural gas, on the other hand, is relatively clean, and the United States produces quite a bit of it, only importing about 16 percent each year. Furthermore, domestic production is expected to continue to rise in the near future, thanks primarily to “unconventional” gas resources. Such unconventional sources were thought to be noncommercial only a few years ago. Recent efforts to pursue these lower-quality reservoirs, which host huge amounts of widely disseminated gas resources, have been remarkably successful.

Today, unconventional natural gas already accounts for one-third of the annual domestic production of the slightly more than 18 trillion cubic feet (Tcf) of natural gas from the lower 48 states, according to DOE. Most unconventional gas is differentiated from traditional natural gas sources in that the gas is produced from reservoir rocks with poor permeability — so poor that drillers must routinely enhance permeability in the rocks surrounding each producing well. Unconventional resources occur in low-permeability sandstones (tight gas), within unusual host rocks such as shales (shale gas) or coal seams (coalbed methane), or within gas hydrates in offshore continental margins and onshore Arctic permafrost. Although the U.S. Energy Information Administration (EIA) and National Petroleum Council foresee slight declines in future production of conventional natural gas in the lower 48 states, both onshore and shallow offshore, unconventional natural gas, as well as deepwater and subsalt offshore gas, will continue to provide a greater share of the overall gas supply in the future.

The Need

Natural gas provides about 22 percent of total U.S. energy needs and is used primarily for industrial fuel and raw materials, electrical power generation and home heating, according to EIA. Natural gas is a cleaner-burning alternative to other fossil fuels used in power generation and can be considered, along with nuclear power and “clean coal” technologies, in near-term carbon-reduction strategies. Natural gas is also the best current starting material for hydrogen manufacture for both industrial use and fuel cells.

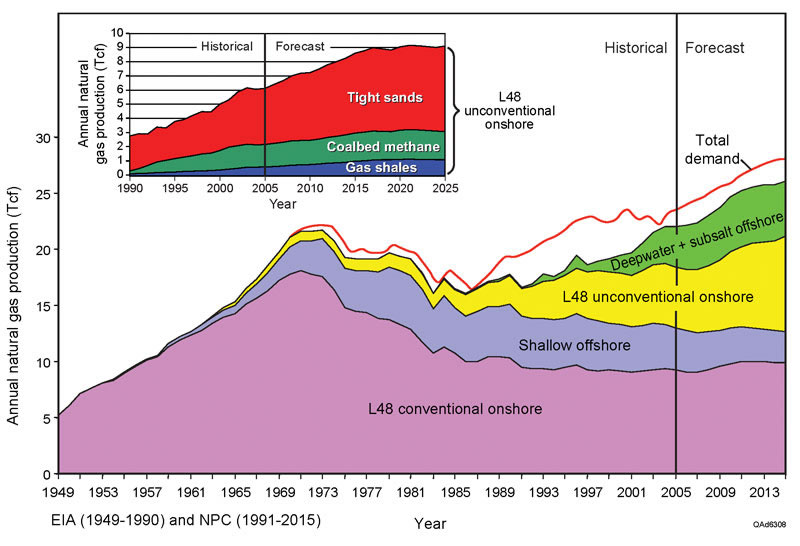

Ambrose, Potter and Briceno: Sources: EIA and NPC

Ambrose, Potter and Briceno: Sources: EIA and NPC

Annual natural gas production in the U.S. lower 48 states in trillion cubic feet. Production from unconventional gas sources (predominantly tight gas) and deepwater/subsalt offshore will continue to increase. In contrast, production from the lower 48 conventional onshore and shallow offshore sources will decline slightly.

Despite abundant natural gas resources and production capacity in the United States, demand still exceeds supply, with the balance imported mostly via pipeline from Canada. The natural gas supply gap will grow to nearly 9 Tcf per year by 2025, according to Michelle Foss at the Center for Energy Economics in Houston, Texas.

Liquefied natural gas (LNG), transported from traditional high-quality reservoirs outside North America, is expected to make up for this growing shortfall. LNG is a form of natural gas that has been refrigerated to reduce volume. It is typically transported to coastal receiving terminals via large, double-hulled transport ships. When giant fields of natural gas are discovered far from markets or pipelines, transport of the gas in LNG form is a common strategy, and this form of international gas trade is growing rapidly. Significant sources of LNG include the Middle East, North and West Africa, the Caribbean, South America, Indonesia, Malaysia and Australia. The United States is expected to increase imports of LNG from 0.6 billion cubic feet per day in 2006 to 9.6 billion cubic feet per day by 2011, according to EIA.

The continuing growth of unconventional domestic gas supplies will lessen the need for LNG. These gas “plays” have already spurred a dramatic rise in drilling activity, with the U.S. gas-rig count surpassing 1,400 since August 2006, double the levels of 2002, according to Jeremy Platt, chair of the Energy Economics Committee of the Energy Minerals Division (EMD) of the American Association of Petroleum Geologists. This upsurge in drilling activity is attributable to rising natural gas prices. The sources of unconventional gas certainly vary, but many are currently economically viable.

The Sources

Unconventional natural gas differs from conventional natural gas and oil systems in terms of its “play elements,” or key geologic attributes. Major play elements for oil and gas deposits include reservoir quality, trap, source and migration. In conventional oil and natural gas deposits, most hydrocarbons originate from organic-rich source beds and migrate into either structural or stratigraphic traps sealed by low-permeability shales, mudstones or salt.

In contrast, unconventional gas systems, such as shale gas and coalbed methane, are self-sourcing, and gas molecules (principally methane) are trapped in pore networks and in adsorbed state on in-situ organic material. Shale gas and coalbed methane production come from a combination of desorbed gas and free gas flowing through fractures (or cleats in coal in the case of coalbed methane), rather than through the types of intergranular pore networks typically encountered in sandstone beds in conventional oil and gas deposits.

Because unconventional gas resources are generally lower-grade compared to conventional gas, more wells — closely spaced over large areas (whole counties or larger) — are required to produce them. Tens of thousands of new wells have been drilled in the United States for unconventional gas in the past decade. Cost-effective exploration and production strategies must take into account the unique set of play elements that exist for each type of unconventional gas reservoir. An in-depth look at the rock properties is vital to understanding the true complexity of these unusual reservoirs.

Tight Gas

Although tight-gas reservoirs — which account for the majority of unconventional U.S. gas production (about 5 Tcf per year) — produce gas from conventional host-rock lithologies (sandstones and limestones), the quality of the reservoir is a major limiting factor for how accessible the gas is. Tight gas reservoirs are commonly so impermeable that fractures, either natural or those that are intentionally induced in the well-completion process, or both, are necessary to boost producibility. Major tight-gas drilling programs are under way in Rocky Mountain basins as well as in eastern and southern Texas.

Stephen Laubach and his team at the Bureau of Economic Geology (BEG) at the University of Texas at Austin are investigating low-permeability sandstones in the deep subsurface and examining links between mechanical and chemical processes in open fractures that can serve as permeability pathways for gas migration to the well bore. Observations of microfractures in thin sections demonstrate that fracturing and mineral cementation are linked processes. Laubach’s team learned that, ironically, fractures can be both clogged (bad news) or propped open (good news) by quartz cementation. Research efforts are now directed at predicting areas of enhanced fracturing where the cracks remain partially open to fluid flow.

Coalbed Methane

Coalbed methane also provides significant contributions to the U.S. unconventional gas supply, accounting for approximately 10 percent of the nation’s methane resources. With at least 750 Tcf of domestic coalbed methane resources recently discovered, more than 550 Tcf of which is in the western United States, coalbed methane production has climbed from negligible amounts in the mid-1980s to almost 2 Tcf per year, according to DOE. Despite this rapid increase, there are indications that production is beginning to flatten, introducing the challenges of searching for new coalbed methane targets and enhancing production in marginal areas.

Coalbed methane production in the United States and Canada is centered in the West.

Coalbed methane has a unique set of factors that affect production, including the type of coal, as well as cleat and fracture development, which together control migration of gas to the well bore. Coal-seam thickness and continuity also play a role in coalbed methane resource size by controlling reservoir volumes and extent. For example, the greatest coalbed methane production in the Cretaceous Fruitland Formation in the San Juan Basin in New Mexico and Colorado coincides with thick coal seams that accumulated landward (southwestward) of ancient shorelines of the shallow sea that once covered this region about 73 million years ago.

Shale Gas

Shale gas plays have recently made a significant impact on unconventional gas production, especially from the Barnett Shale in the Fort Worth Basin in Texas, where estimated resources are approximately 26 Tcf, according to the U.S. Geological Survey. The Fort Worth Basin is one of about 20 shale gas basins across the United States where total domestic shale gas resources are thought to range from 500 Tcf to 780 Tcf, according to Schlumberger, Inc.

Despite this enormous resource, the percentage of gas recovered by today’s production methods in shale gas reservoirs is low (typically less than 15 percent of estimated gas in place), and controls on shale gas producibility and recovery are still not well-understood. Work continues on modeling fluid flow in nanometer-scale pores in shale gas reservoirs, where classical equations that describe fluid flow through porous media may not be valid, according to Farzam Javadpour at the Alberta Research Council in Canada.

Shale gas research is expanding rapidly as a result of successes in the Barnett in Texas and the age-equivalent Fayetteville Shale in northern Arkansas, and the push to repeat those successes elsewhere. This research covers a wide spectrum of issues. Fundamental depositional controls on mudstones are being reexamined by geologists such as Juergen Schieber at Indiana University in Bloomington. Other major areas of study include pore and fracture development, physical rock properties of shales, and burial/thermal history with related hydrocarbon expulsion. All of these areas of research will help determine production strategies during the lifetime of shale gas plays, targeting recovery of a larger fraction of in-place resources.

Still, there are challenges to this production. The need for safe and efficient disposal of waste water produced during production can be a significant cost factor for producing both coalbed methane and shale gas. Many coalbed methane wells (for example, in the Powder River Basin in Wyoming) require the production of substantial volumes of water before methane becomes mobile and migrates to the well bore. Water is commonly used to fracture the rocks to enhance production in shale gas reservoirs such as the Barnett Shale, where an individual horizontal well can require up to 3 million gallons of water for multiple “frac jobs” in the well-completion process. The Railroad Commission of Texas reports that about 2.6 billion gallons of water were used for frac jobs in the Barnett Shale in 2006. Basinwide, this amounts to 2 percent of total water usage, but in some areas in the Fort Worth Basin, frac water is 10 to 20 percent of the local usage from the Trinity aquifer, according to Jean-Philippe Nicot of BEG. Most of this frac water is produced with the gas and must be disposed of by deep injection. One implication for the oil and gas industry, particularly in the Barnett Shale play, is that operators may eventually have to rely on fracturing techniques that use reconditioned, produced water or less water in general.

Gas hydrates —The New Frontier

Although commercial production has already been established from shale gas and coalbed methane, gas hydrates are truly a frontier resource. Hydrates occur predominantly as methane trapped inside ice-lattice molecular structures in deepwater seafloor sediments. Because of the high-pressure and low-temperature conditions of the seafloor, hydrate methane is a concentrated energy source, with an energy density of 42 percent of that of LNG, according to Bob Hardage of BEG. Although estimates of gas-hydrate resources are uncertain, many experts think that these resources are enormous, and the potential North American resource may be many thousands of trillion cubic feet.

Although natural gas from hydrates is not yet economically feasible to produce, it has been produced successfully in pilot wells in permafrost regions of Russia and Canada. Lessons learned from these investigations could result in viable commercial production by 2015, according to Art Johnson, chair of the EMD Gas Hydrates Committee. However, several safety and technical issues need to be resolved before gas hydrates can become a viable source of unconventional gas. For example, seafloor stability must be assured, as large-scale slumping of shallow, hydrate-bearing strata during production could potentially damage production facilities and release large amounts of methane into the water column and eventually into the atmosphere. Methane, volume-for-volume, is about 20 times more potent than carbon dioxide as a greenhouse gas, so unintended releases must be guarded against.

Important technical issues for gas hydrates include the need for improved petrophysical characterization — a difficult proposition, however. The three-dimensional distribution of gas hydrates can be complex, occurring either in disseminated or tabular form. Realistic modeling of this distribution has a significant bearing on an accurate determination of gas saturation and, thus, on potential resource size. One step in determining distribution of hydrates in sediments involves the correlation of gas-hydrate rock properties with seismic data.

The Future

Obviously, there are several sources of natural gas that are markedly different from conventional gas that may stave off some of the energy issues the United States will face in the coming years. The new unconventional sources are lower-grade, but very widespread in U.S. sedimentary basins. Natural gas consumption in the United States will continue to grow, driven by demand for electric power, home heating, industrial uses and cleaner-burning alternatives to oil and coal for transportation and electricity.

LNG imports, which EIA anticipates will grow from 1 percent of the U.S. natural gas supply to approximately 15 percent by 2025, will help to meet future demands. As these LNG imports come online, additional natural gas production from unconventional gas plays will help to fill supply gaps for the next several decades.

Ambrose, Potter and Briceno are all at the Bureau of Economic Geology at the University of Texas at Austin. The authors gratefully acknowledge Joel Lardon, who drafted the second figure, and Lana Dieterich, who helped edit the manuscript.

{kind=link}

No comments:

Post a Comment